In this Edition

- The ups and downs of the M&A and financing markets in the emerging companies and venture capital sector.

- New export controls on technology and tariffs on imported goods, federal amendments that target “greenwashing,” tips on starting a company in the life sciences sector, and other need-to-know topics.

- Startup deals have been steadily declining since 2021, but there may be hope that things turn around soon.

Market Insights

“Dual Track” Process: Maintaining Transaction Flexibility to Optimize Value — The ups and downs of the M&A and financing markets over the past few years, particularly in the emerging companies (EC) and venture capital (VC) sector, have demonstrated the importance of emerging companies and their stakeholders maintaining flexibility when pursuing liquidity transactions. Running a “dual track” process, or the parallel pursuit of both an M&A transaction and a financing transaction, such as an initial public offering (IPO), can be an effective strategy to maximize transaction certainty and optimize valuations.

Read more in our new Blakes Bulletin: “Dual Track” Process: Maintaining Transaction Flexibility to Optimize Value.

Legal Update

Founders and investors may find the following insights from our Blakes colleagues helpful and instructive:

- Starting up in Life Sciences — Starting a company in the life sciences sector comes with its unique set of challenges and learning opportunities. From establishing a solid foundation built on a strong business case and clear legal documentation to effectively engaging your investor base, each step of the formation process requires careful consideration and strategic planning. Learn more about these steps in our Blakes Five Under 5: Key Tips for Building a Successful Life Sciences Company.

- Technology Exports — In a significant move, Canada has announced stringent export controls on certain quantum computing and advanced semiconductor technology under the Export and Import Permits Act (EIPA). Beginning on July 20, 2024, the export of certain technology related to quantum computing and advanced semiconductors will be prohibited to any location except the United States without an export permit from Global Affairs Canada. Learn more about these new export controls in our Blakes Bulletin: Canada Imposes Export Controls on Quantum Computing and Advanced Semiconductor Technology.

- Digital Services Tax — Despite significant political headwinds, particularly from the United States, Canada’s digital services tax (DST) was enacted pursuant to an order-in-council dated June 28, 2024. Taxpayers’ DST liability for 2024 will include DST applicable to digital revenues from 2022 and 2023. Read more in our Blakes Bulletin: Canada Enacts Digital Services Tax and Other Significant Tax Measures.

- Greenwashing Amendments to the Competition Act — The federal government passed amendments to the Competition Act (Act) that target “greenwashing” (i.e., making untested or unsubstantiated claims about the environmental benefits of a product or business). These amendments create substantial uncertainty, risks and potential liability for businesses, which could undermine the environmental initiatives of Canadian corporations. Learn more about these amendments in our Blakes Bulletin: Canada’s New Greenwashing Laws Enacted.

- New Tariffs on Chinese Imports — On August 26, 2024, the Canadian government announced significant measures impacting importations of Chinese goods. The new and proposed surtaxes on sectors critical to Canada’s manufacturing industry and “net-zero transition” will impact a wide swath of Canadian businesses. Learn more about these new tariffs in our Blakes Bulletin: Canada Introduces New Tariffs on Chinese EVs and Steel Products.

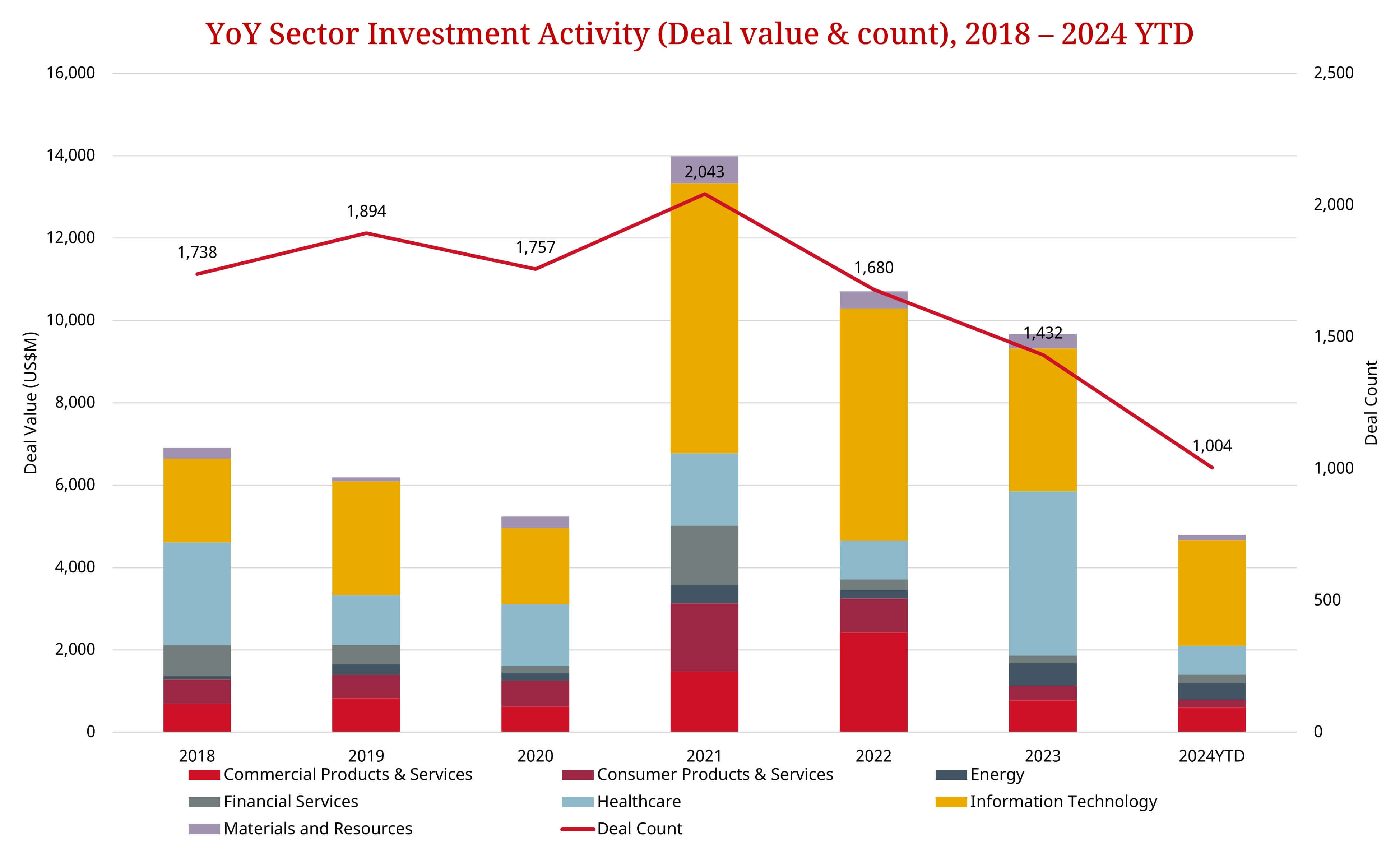

Deal Monitor

Data sourced from PitchBook.

- Early-stage deal value is down 26% from June, and later-stage deal value is down 20% in that same time. There were no growth equity deals in January – June 2024, but now growth equity comprises 46% of the total 2024 YTD deal value.

- IT investments continue to be the most active industry, comprising 40% of the top 20 deals and 53% of total deals. Healthcare investments, which had been slow in the first half of 2024, have picked up in recent months comprising 15% of total deals in 2024 YTD, which we forecasted in the last edition. Financial Services, which had been active in the first half of 2024, has slowed down while Commercial Products & Services has picked up, comprising 13% of total deals.

- Among the largest transactions was Quebec-based SOFIAC’s strategic partnership with Fondaction, Mirova and ADEME Investissement, including EUR $60-million (roughly C$90.5-million) funding to develop an innovative investment model intended to accelerate the energy transition and decarbonization of Canadian businesses.

- Other notable transactions in 2024 include Ideogram’s C$80-million Series A funding led by Andreessen Horowitz; Taalas’ US$50-million funding from Quiet Capital and Pierre Lamond; and UniUni’s Series C US$50-million funding led by DCM Ventures.

- Although we’ve been seeing a steady decline in the number of deals since 2021, there is new hope that the venture market will recover based on a combination of factors, including the declining cost of capital resulting from lower interest rates, improved macro and liquidity conditions, accelerated technological advancements and a surge in entrepreneurial ambition.

Contact Us

If you have any questions, please contact any member of our Emerging Companies & Venture Capital group.

For our recent publicly available experience, visit our website.