On October 9, 2024, as part of its C$160 billion net-zero economic plan, the Government of Canada announced various initiatives to expand the coverage of mandatory climate disclosure requirements to large, federally incorporated private companies and develop a sustainable finance taxonomy. The aim of these initiatives is to mobilize the private investment needed for Canada to reach its net-zero emissions target by 2050, notably by providing investors seeking sustainable options with the clarity they need, while capitalizing on major economic opportunities.

Mandatory Climate-Related Financial Disclosures for Large, Federally Incorporated Private Companies

The federal government plans to amend the Canada Business Corporations Act to require climate-related financial disclosures for large, federally incorporated private companies, with disclosure requirements already in place for federal Crown corporations and federally regulated financial institutions. The substance of these disclosure requirements and the size of private federal corporations that would be subject to them will be determined through a regulatory process. The government will seek to harmonize its regulations with those that will be required from public companies by securities regulators (see our March 2024 Blakes bulletin: New Developments in the Sustainability Disclosure Landscape).

Increased disclosure is intended to keep Canada’s largest corporations competitive in attracting capital in the context of an international movement towards net-zero. The aim is to provide investors with a better understanding of how large, federally incorporated private companies approach and manage climate-related risks, so they can be more confident in their capital allocation being in line with the realities of a zero-emissions economy.

While small and medium-sized businesses will not be required to comply, the federal government is exploring ways to encourage them to voluntarily disclose climate-related information.

Made-in-Canada Sustainable Investment Guidelines

Building on the recommendations of the Sustainable Finance Action Council, the federal government is advancing the development of voluntary guidelines for sustainable investment in Canada, which will be developed and governed by an external, third-party organization, with the federal government funding the technical work.

This taxonomy’s main objective is to identify and classify investments which, on the basis of scientifically determined criteria, are compatible with the goal of net-zero emissions by 2050 and limiting the global temperature increase to 1.5°C above pre-industrial levels (i.e., low or zero-emission activities or those that support them, referred to as “green,” and activities designed to support the decarbonization of emissions-intensive sectors, referred to as “transition”). It will provide stakeholders with clarity on what constitutes sustainable activities in the interests of mobilizing investment towards these activities. To this end, the taxonomy will be developed according to guiding principles that ensure it is usable, credible, comprehensive, interoperable, transparent, dynamic and holistic.

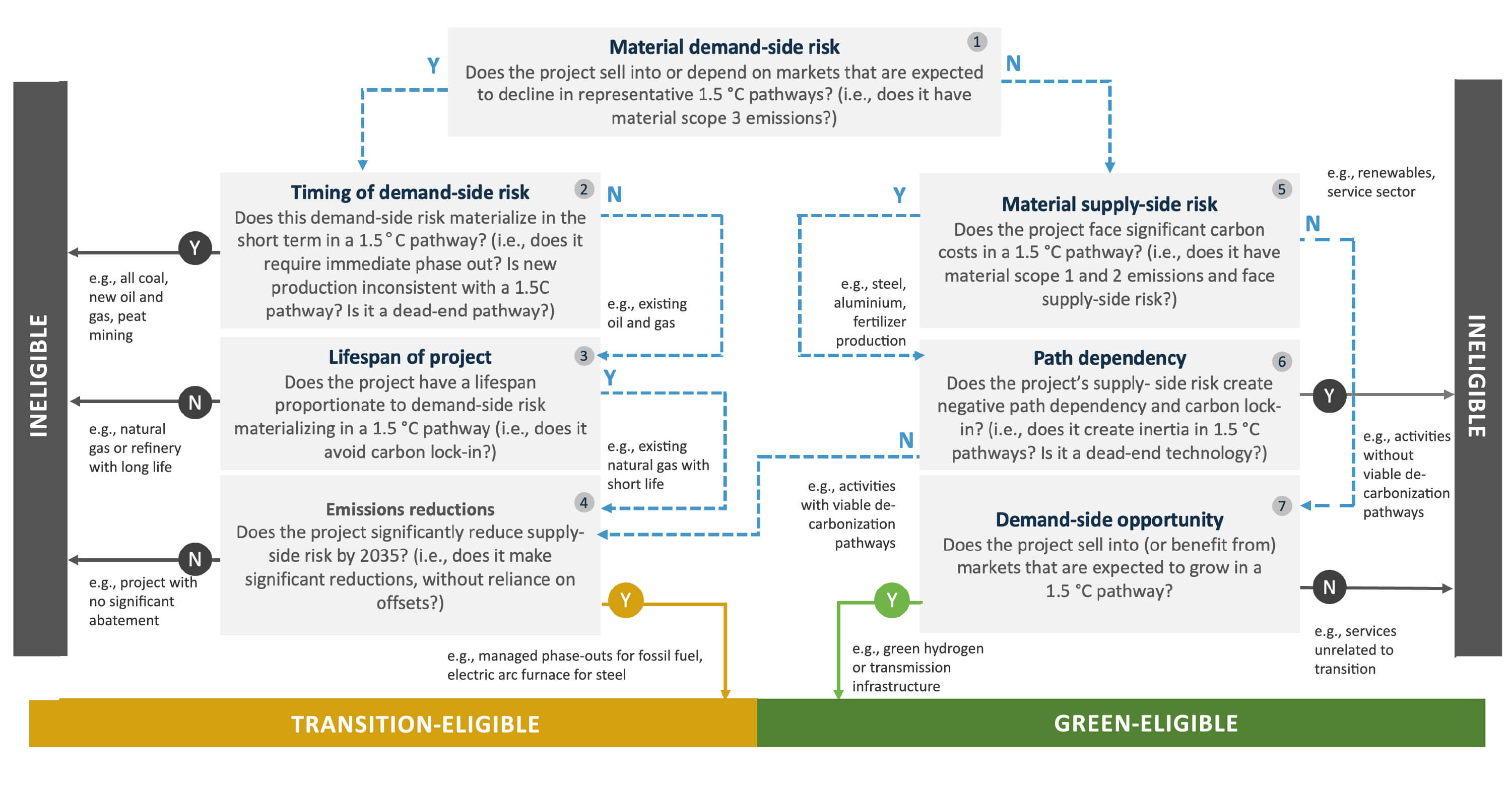

The figure below illustrates the framework proposed by the Sustainable Finance Action Council that will likely guide the development of the taxonomy.

The Canadian taxonomy will initially focus on certain eligible activities in Canadian sectors of general importance to Canada’s economic landscape and its decarbonization, among others, while aligning with international standards. These activities will be identified by an external, third-party organization, that will prioritize two or three sectors within 12 months of the start of the third-party organization’s work.

Activities that could be targeted include power generation from renewable sources, low-emission transportation infrastructure, energy-efficient buildings, sustainable agriculture and forestry practices, and other activities in heavy industries such as manufacturing, mining and natural gas extraction.

Provided that eligible activities are carried out in accordance with their specific performance criteria and Do-No-Significant-Harm requirement (the latter requirement being designed to avoid narrow investments that privilege one environmental or social objective over others, potentially neglecting areas such as water, waste and biodiversity management), companies conducting these activities will qualify for a “green” or “transition” label.

The third-party organization will make the final determination of guiding principles, eligible activities, priority sectors and company-level expectations, which could include the adoption of net-zero targets, credible transition plans and rigorous climate disclosure.

In preparation for these initiatives, companies should closely examine their climate change monitoring, reporting and compliance mechanisms and risk management integration.

We will continue to monitor developments and provide updates as appropriate. For more information, please contact the authors or any other member of our Corporate Governance or Environmental, Social & Governance (ESG) groups.